Was The June FOMC Meeting A Fed Pause Or Hawkish Skip?

The announcement made it clear that the committee still needs more compelling evidence that inflation is under control and could very well tighten at least once more this summer.

For the first time since January 2022, the Federal Open Market Committee (FOMC) voted to leave the Federal funds rate unchanged at a target range of 5.00%-5.25% at its June meeting. While this “pause” had been telegraphed by Federal Reserve (Fed) officials in recent weeks, the statement language and press conference commentary were decisively hawkish. The statement was essentially unchanged except for a slight adjustment from “to which” to “of” in “determining the extent of additional policy firming that may be appropriate”, suggesting another increase is to be expected. Moreover, in his remarks Chair of the U.S. Fed, Jerome Powell, confirmed the committee used the June meeting to assess the impact of the cumulative tightening since the Fed began hiking in March of last year though hinted that while the trends in inflation and labor markets were encouraging, they are still at levels that warrant further tightening.

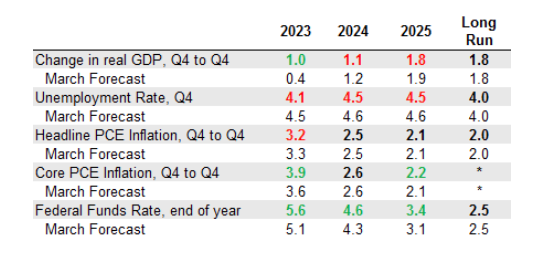

Turning to the Summary of Economic Projections (SEP), there were some notable adjustments to the economic forecasts relative to the last meeting:

The 2023 real GDP forecast was revised up 0.6% to 1.0%, but remained largely unchanged for the remainder of the forecast period

The 4Q23 unemployment rate was revised lower by 0.4% to 4.1%, suggesting continued resilience in the labor market even amid the expectation of sub-trend growth

Headline PCE inflation was trimmed to 3.2% while core inflation was revised 0.3% higher to 3.9% in the fourth quarter

The refreshed SEP suggests a soft landing is still in the cards though inflation will remain stubbornly elevated. Perhaps more notable was the updated “dot” plot. Of the 18 FOMC members, nine see rates ending the year between 5.5-5.75%, while three see rates above 5.75%. This now suggests the median FOMC member anticipates two more rate increases, indicating the mid-year meeting will serve as hawkish skip and not a pause in the current tightening cycle.

To be clear, we do not think further tightening is appropriate at this stage given growth is slowing and labor markets are already loosening. Moreover, we anticipate another soft inflation print for June driven by base effects, normalizing rent inflation and used car prices. That said, today’s announcement made it clear that the committee still needs more compelling evidence that inflation is under control and could very well tighten at least once more this summer.

Equities and bonds sold off initially as rates moved higher. While a soft landing is still possible, additional tightening reduces that likelihood as more rate rises will further exacerbate the challenges facing the banking sector and add more pressure on consumers and businesses.

FOMC June 2023 Forecasts

Percent

Source: Federal Reserve, J.P. Morgan Asset Management. Data are as of June 14, 2023. Forecasts of 18 FOMC participations, median estimate. Green denotes an adjustment higher, red denotes an adjustment lower. * Longer-run projections for core PCE inflation are not collected.